All Categories

Featured

Table of Contents

Numerous whole, universal and variable life insurance plans have a money worth part. With one of those policies, the insurer deposits a part of your regular monthly premium settlements right into a cash money worth account. This account earns passion or is spent, helping it expand and give an extra significant payout for your recipients.

With a degree term life insurance coverage policy, this is not the case as there is no cash value component. As an outcome, your plan will not grow, and your fatality advantage will certainly never increase, consequently limiting the payment your beneficiaries will certainly obtain. If you want a policy that gives a survivor benefit and builds cash money worth, consider entire, universal or variable strategies.

The 2nd your policy ends, you'll no much longer live insurance protection. It's typically feasible to renew your plan, yet you'll likely see your premiums increase significantly. This can provide concerns for retired people on a set revenue since it's an extra cost they may not have the ability to manage. Level term and reducing life insurance policy deal comparable policies, with the primary distinction being the survivor benefit.

(EST).2. On-line applications for the are readily available on the on the AMBA site; click the "Apply Now" blue box on the best hand side of the web page. NYSUT members can additionally print out an application if they would certainly prefer by clicking the on the AMBA site; you will certainly then need to click on "Application Type" under "Kinds" on the right-hand man side of the page.

How do I apply for Level Term Life Insurance Vs Whole Life?

NYSUT participants enrolled in our Level Term Life Insurance Policy Strategy have accessibility to provided at no extra cost. The NYSUT Member Conveniences Trust-endorsed Degree Term Life Insurance Policy Plan is financed by Metropolitan Life insurance policy Company and provided by Association Member Advantages Advisors. NYSUT Trainee Members are not qualified to take part in this program.

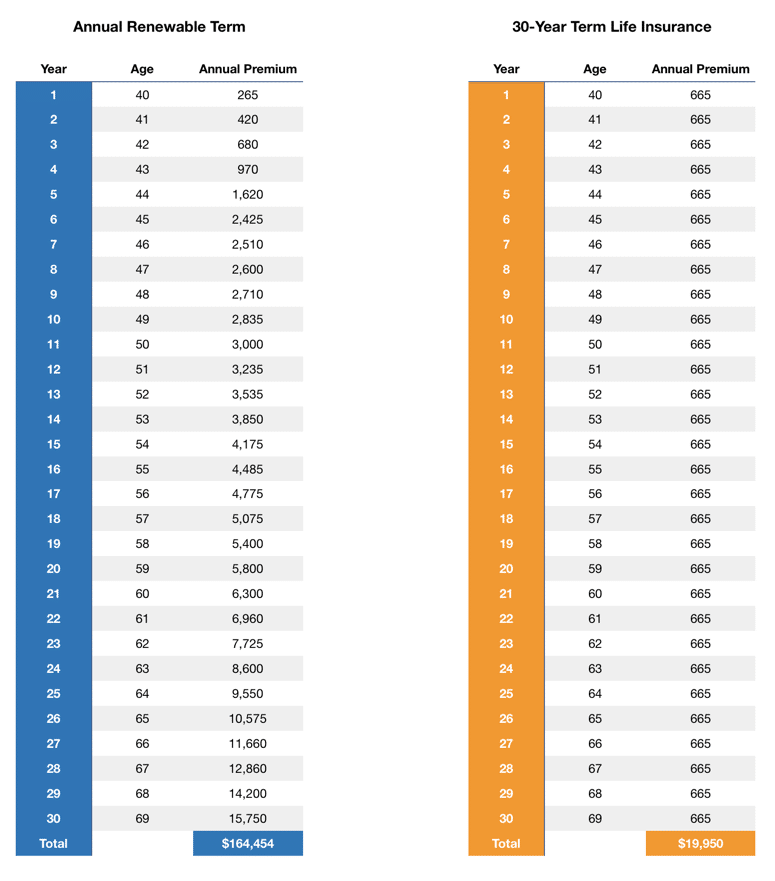

Term life insurance policy is a cost effective and simple alternative for lots of people. You pay premiums on a monthly basis and the protection lasts for the term size, which can be 10, 15, 20, 25 or three decades. But what takes place to your premium as you age depends on the kind of term life insurance policy protection you acquire.

As long as you remain to pay your insurance coverage costs each month, you'll pay the exact same rate throughout the entire term length which, for lots of term policies, is normally 10, 15, 20, 25 or 30 years (Best level term life insurance). When the term finishes, you can either pick to finish your life insurance policy coverage or renew your life insurance policy plan, usually at a higher rate

Who offers flexible No Medical Exam Level Term Life Insurance plans?

For example, a 35-year-old female in outstanding health and wellness can purchase a 30-year, $500,000 Haven Term plan, provided by MassMutual beginning at $29.15 per month. Over the next 30 years, while the policy remains in place, the price of the coverage will certainly not change over the term period. Allow's encounter it, the majority of us do not such as for our expenses to expand over time.

Your level term rate is identified by a variety of elements, most of which are relevant to your age and health and wellness. Various other elements include your particular term plan, insurance service provider, advantage amount or payout. Throughout the life insurance policy application process, you'll respond to questions regarding your wellness history, consisting of any kind of pre-existing problems like an important health problem.

Remember that it's constantly very important to be honest in the application process. Issuing the policy and paying its advantages depends upon the applicant's proof of insurability which is figured out by your solution to the health and wellness questions in the application. A clinically underwritten term policy can secure an inexpensive rate for your coverage duration, whether that be 10, 15, 20, 25 or three decades, no matter how your wellness could change throughout that time.

With this sort of degree term insurance coverage, you pay the very same regular monthly costs, and your beneficiary or beneficiaries would receive the same advantage in case of your death, for the entire insurance coverage duration of the plan. Just how does life insurance work in terms of cost? The expense of level term life insurance policy will rely on your age and wellness in addition to the term size and coverage quantity you pick.

Where can I find Low Cost Level Term Life Insurance?

Life: AgeGenderFace AmountTerm LengthPremium30Male$500,00030$29.9930 Female$1,000,00030$43.3135 Male$500,00020$20.7235 Women$750,00020$23.1340 Male$600,00015$22.8440 Women$800,00015$27.72 Price quote based on rates for qualified Haven Simple candidates in excellent wellness. Rates distinctions will certainly vary based on ages, health status, insurance coverage amount and term length. Haven Simple is presently not offered in DE, ND, NY, and SD.Regardless of what insurance coverage you choose, what the policy's money worth is, or what the swelling amount of the death advantage becomes, satisfaction is amongst the most useful advantages connected with acquiring a life insurance coverage plan.

Why would certainly someone select a policy with a yearly renewable costs? It might be a choice to take into consideration for a person who needs coverage just briefly. An individual who is in between jobs yet desires fatality advantage security in place because he or she has financial obligation or various other economic commitments may intend to think about an each year sustainable plan or something to hold them over up until they start a brand-new task that offers life insurance policy - 30-year level term life insurance.

You can generally renew the policy yearly which gives you time to consider your alternatives if you desire protection for longer. That's why it's handy to acquire the right amount and size of insurance coverage when you first get life insurance, so you can have a reduced price while you're young and healthy and balanced.

If you contribute important overdue labor to the household, such as day care, ask yourself what it may cost to cover that caretaking job if you were no more there. Make sure you have that coverage in area so that your family members gets the life insurance benefit that they need.

Low Cost Level Term Life Insurance

Does that indicate you should constantly select a 30-year term length? In general, a much shorter term policy has a reduced premium price than a much longer plan, so it's wise to choose a term based on the predicted size of your economic duties.

These are all essential variables to maintain in mind if you were considering choosing a long-term life insurance policy such as a whole life insurance coverage plan. Many life insurance policy plans offer you the choice to add life insurance riders, believe added advantages, to your policy. Some life insurance policy policies feature motorcyclists built-in to the price of premium, or cyclists may be offered at an expense, or have costs when worked out.

With term life insurance policy, the interaction that many people have with their life insurance policy firm is a monthly bill for 10 to 30 years. You pay your monthly costs and wish your family members will never need to use it. For the group at Haven Life, that looked like a missed out on possibility.

{kind=link}

Latest Posts

All Life Funeral Insurance

Open Care Final Expense Plans Reviews

Funeral Insurance California